Freelancer 15% regime in Moldova (independent entrepreneur)

04.03.2026

Starting January 1, 2026, the Republic of Moldova introduced a new tax regime for people who work on their own: the “independent entrepreneur” (freelancer) status, with a single tax of 15% (within certain limits).

The regime was introduced by Law No. 228/2025 and is designed for independent activities, with simpler procedures and digital administration.

What is an “independent entrepreneur” and who can use it?

The law defines an independent entrepreneur as a resident individual who carries out an independent economic activity individually in the fields listed in the annex, without opening a company (SRL, ÎI, etc.).

The regime applies exclusively to independent economic activities within the scope provided by the law.

Which activities are eligible?

The regime applies only to service activities included in the legal list (CAEM). Below is the full list used for this regime:

PROGRAMMING, IT & ONLINE.

- 62.01 – Custom software development (client-oriented software).

- 62.02 – Information technology consultancy activities.

- 63.1 – Web portals, data processing, web hosting/administration and related activities.

- 63.11 – Data processing, web hosting/administration and related activities.

- 63.12 – Web portals.

- 63.91 – News agency activities.

MARKETING, PR & MARKET RESEARCH.

- 70.21 – Public relations and communication consultancy activities.

- 73.20 – Market research and public opinion polling.

DESIGN, PHOTO, TRANSLATION & CREATIVE ARTS.

- 74.1 – Specialized design activities.

- 74.2 – Photographic activities.

- 74.3 – Translation and interpreting activities.

- 90.01 – Performing arts.

- 90.02 – Support activities to performing arts.

- 90.03 – Artistic creation.

MEDIA, PUBLISHING & ENTERTAINMENT.

- 58.1 – Book, newspaper and magazine publishing and other publishing activities.

- 58.11 – Book publishing.

- 58.12 – Publishing of directories and mailing lists and similar publications.

- 58.13 – Publishing of newspapers.

- 58.14 – Publishing of journals and periodicals.

- 58.19 – Other publishing activities.

- 58.2 – Software publishing.

- 58.21 – Publishing of computer games.

- 58.29 – Other software publishing.

- 59.1 – Motion picture, video and television programme production.

- 59.11 – Motion picture, video and television programme production.

- 59.12 – Motion picture, video and television programme post-production activities.

- 59.13 – Motion picture, video and television programme distribution activities.

- 59.14 – Motion picture projection activities.

- 59.2 – Sound recording and music publishing activities.

- 71.11 – Architectural activities.

- 71.12 – Engineering activities and related technical consultancy.

TOURISM.

- 79.9 – Other reservation services and related activities.

EDUCATION / TRAINING (OTHER FORMS OF EDUCATION).

- 85.5 – Other education.

- 85.51 – Sports and recreation education.

- 85.52 – Cultural education (music, theatre, dance, visual arts, etc.).

- 85.53 – Driving schools.

- 85.59 – Other education n.e.c.

CLEANING & LANDSCAPING.

- 81.2 – Cleaning activities.

- 81.21 – General cleaning of buildings.

- 81.22 – Other building and industrial cleaning activities.

- 81.29 – Other cleaning activities n.e.c.

- 81.3 – Landscape service activities.

SECRETARIAL SERVICES & EVENT ORGANIZATION.

- 82.19 – Photocopying, document preparation and other specialized office support activities.

- 82.3 – Organization of conventions and trade shows.

SOCIAL ASSISTANCE (WITHOUT ACCOMMODATION).

- 88.9 – Other social work activities without accommodation.

- 88.91 – Child day-care activities.

- 88.99 – Other social work activities without accommodation n.e.c.

SPORTS.

- 93.11 – Operation of sports facilities.

- 93.12 – Activities of sports clubs.

- 93.19 – Other sports activities.

PERSONAL SERVICES.

- 96.09 – Other personal service activities n.e.c. (excluding pet care and porters).

REPAIRS / TECHNICAL MAINTENANCE (INDUSTRIAL).

- 33.1 – Repair of fabricated metal products, machinery and equipment.

- 33.11 – Repair of fabricated metal products.

- 33.12 – Repair of machinery.

- 33.13 – Repair of electronic and optical equipment.

- 33.14 – Repair of electrical equipment.

- 33.15 – Repair and maintenance of ships and boats.

- 33.16 – Repair and maintenance of aircraft and spacecraft.

- 33.17 – Repair and maintenance of other transport equipment.

- 33.19 – Repair of other equipment.

CONSTRUCTION – INSTALLATIONS (HVAC / SANITARY / GAS).

- 43.22 – Plumbing, heat and air-conditioning installation.

PRODUCTION / CRAFTS (MANUFACTURING) LEATHER / LEATHER GOODS.

- 15.1 – Tanning and dressing of leather; manufacture of luggage, handbags, saddlery and harness; dressing and dyeing of fur.

- 15.11 – Tanning and dressing of leather; dressing and dyeing of fur.

- 15.12 – Manufacture of luggage, handbags and the like, saddlery and harness.

GLASS / CERAMICS.

- 23.13 – Manufacture of hollow glass.

- 23.41 – Manufacture of ceramic household and ornamental articles.

- 23.44 – Manufacture of other technical ceramic products.

- 23.49 – Manufacture of other ceramic products n.e.c.

JEWELRY / INSTRUMENTS / GAMES & TOYS / SPORTS GOODS.

- 32.1 – Manufacture of jewelry, imitation jewelry and related articles.

- 32.11 – Striking of coins.

- 32.12 – Manufacture of jewelry and related articles.

- 32.13 – Manufacture of imitation jewelry and related articles.

- 32.2 – Manufacture of musical instruments.

- 32.3 – Manufacture of sports goods.

- 32.4 – Manufacture of games and toys.

Basic conditions

- You must be a resident individual in Moldova.

- You are at least 18 years old.

- You work on your own (no employees under this status).

How does the 15% tax work?

The regime follows a simple logic:

- 15% single tax if the annual income does not exceed 1,200,000 lei.

- 35% on the portion that exceeds the 1,200,000 lei cap.

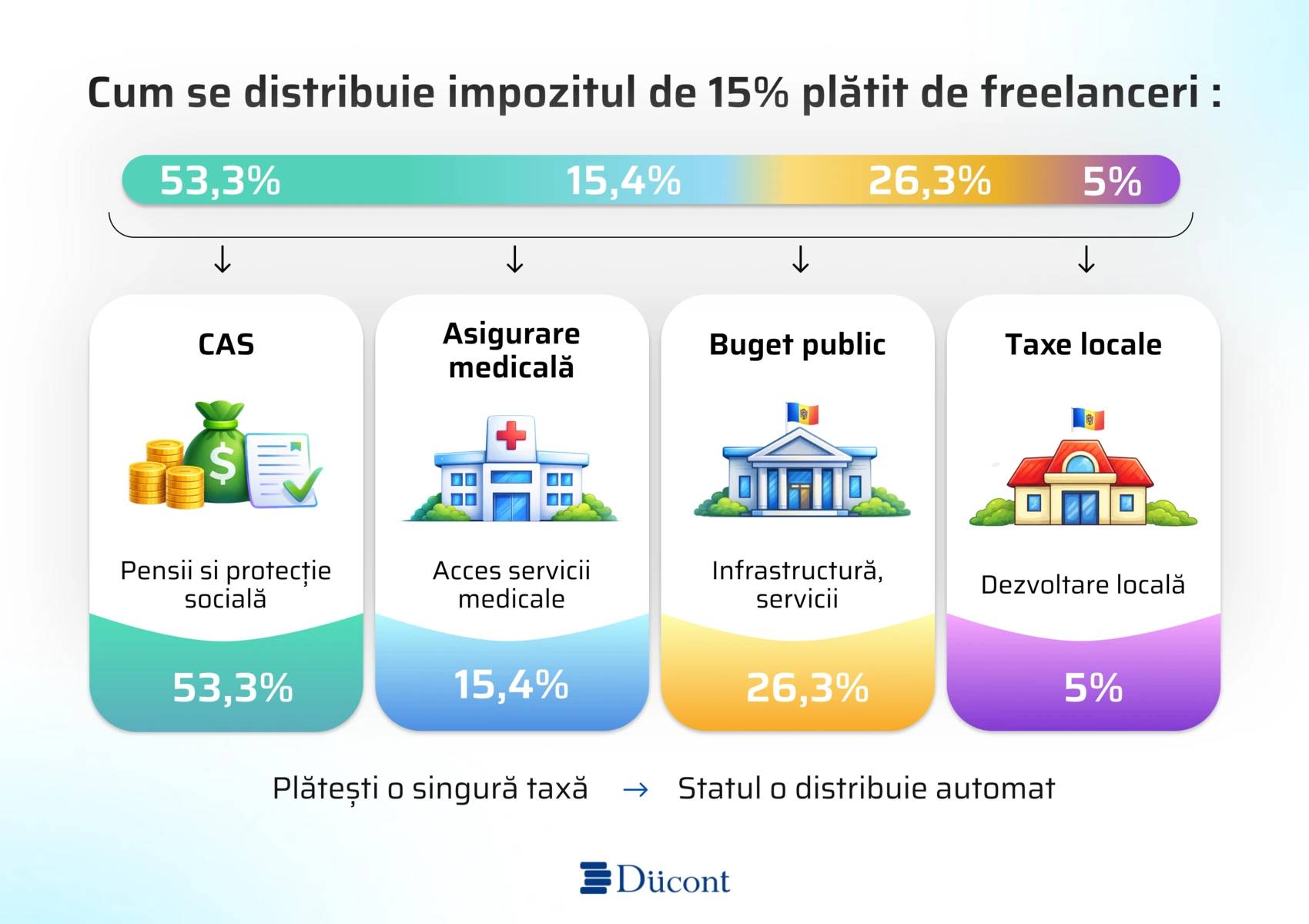

What does this 15% include?

The single tax is not just “income tax”. It includes:

- Income tax.

- Social contributions (CNAS).

- Health insurance (AOAM).

- Local taxes.

The law also shows how the amount is allocated.

- 26.3% for income tax.

- 5.0% to the local budget (local taxes).

- 53.3% to the social insurance budget.

- 15.4% to AOAM funds (health insurance).

How to register as a freelancer in Moldova?

Registration is online, free of charge and done via EVO (digital ecosystem) / ASP, using an electronic signature.

What do you need?

- Electronic signature.

- Access to EVO.

- Submit the application and sign electronically.

- Open dedicated bank accounts for the independent entrepreneur activity.

Records, payments and fiscal receipt: what changes in practice.

This is one of the biggest differences compared to classic business forms. Independent entrepreneurs:

- Do not keep accounting records.

- Do not file tax or statistical reports/returns.

Records are kept by the SFS based on:

- Data from cash register equipment (if you collect cash).

- Data from the current accounts dedicated to the activity (bank accounts opened specifically for this activity).

When do you need a cash register?

- If you collect cash, you must use cash register equipment and issue a fiscal receipt.

- If you collect income by bank transfer.

- For non-cash payments (e.g., MIA / card / transfer), you do not have the same receipt obligation as for cash.

How and when do you pay the tax?

The system is designed to be administered by the SFS:

- The SFS calculates the tax monthly and sends a payment notice.

- The notice arrives by the 10th of the following month.

- Payment is due by the 25th of the following month./

Social and health benefits: what you get in return.

The new regime is not just a “simple tax”. It is also linked to social protection. Independent entrepreneurs can benefit from:

- Temporary disability allowance.

- Maternity allowance.

- Family/child allowances.

- Paternity allowance.

- Pension rights (based on contributions).

For 2026, if the AOAM (health insurance) component within the single tax does not cover the minimum fixed amount, the difference must be paid (2,527 lei). Based on our freelancer calculator, we estimated that an independent entrepreneur’s income should be >110,000 lei per year for the paid taxes to fully cover the health insurance.

What should you check before registering?

- The exact CAEM code (not only the commercial description of the service).

- How you will get paid (cash, bank account, card, etc.).

- What is most tax-efficient for you, depending on your field and income level, can be checked using our other calculators.

IT PARK vs Freelancer

Compare taxes and contributions between the IT Park regime and the independent entrepreneur regime (15% freelancer).

Calculate nowSRL vs IT Park

See the difference in taxation between a classic SRL and the IT Park tax regime.

Calculate nowSRL vs II

Compare taxes, contributions and administrative costs between SRL and Întreprinzător Individual to choose the right legal form.

Calculate nowIn conclusion, the new tax regime for independent entrepreneurs is an efficient and advantageous option for smaller incomes. For higher incomes, IT Park or an SRL is usually more suitable. You can contact us for a free consultation, and we will recommend the best option for your case.